Payment Processing Tools for Media Production Workflows

Payment processing in media production is not one workflow. It is a cluster: vendor invoice payments (ACH, wire, check), contractor payouts, crew reimbursements, international vendor FX, card funding, per diem distributions, and payroll disbursement. Most of these are handled by different tools on the same production. This guide covers the leading payment processing tools for media production workflows in 2026, what each category is for, and how they fit into the broader production finance stack.

The distinct payment types in production

Unlike most businesses, a production processes four structurally different payment categories, often in a single week:

- Vendor invoices. Equipment houses, catering, post facilities, music clearance. Typically ACH or check, sometimes wire for large invoices.

- Contractor payouts. 1099 payments to freelance crew, musicians, artists. ACH most common, corp-to-corp wires for loan-outs.

- Crew reimbursements. Small out-of-pocket spend reimbursed to crew members. Often via production cards replacing reimbursement workflows entirely.

- Payroll. W-2 wages, fringe contributions, and related payments. Handled by a payroll firm (Wrapbook, Cast and Crew, EP, GreenSlate), not the production directly.

Each category has different compliance, timing, and integration needs. Running them all through one general payment processor (Stripe, Square, PayPal) leaves most of them poorly served.

What to look for in production payment tools

Production chart of accounts coding

Payments should code to the production chart of accounts on the way out, not get reconciled afterward. A vendor payment for grip equipment should post to the grip line automatically, not flow through a generic "equipment" bucket that a production accountant has to split.

Three-way matching with POs and receipts

For vendor invoices, payment should only release after the invoice matches an approved PO and a delivery confirmation. See our purchase orders guide for how this works.

Configurable approval workflows

A payment over a threshold should route to a producer or UPM for approval. Below the threshold, it can auto-release after three-way match. Thresholds should be configurable per show.

Fast payment rails

Production cashflow does not wait. Same-day ACH, RTP (real-time payments), and late wire cutoffs matter. Traditional banks with 2 PM wire cutoffs often cause Friday-afternoon payment delays that push into Monday.

International FX and payment methods

Productions with international shoots need SWIFT wires, multi-currency accounts, and competitive FX (near mid-market rates, not 2 to 3 percent markup). Some platforms also support local payment methods (SEPA in EU, Interac in Canada, PIX in Brazil).

Vendor onboarding integration

Payments should be gated on complete vendor onboarding. Missing W-9 means no payment. Expired COI means payment holds. This prevents 1099 scramble at year end and contractual compliance gaps.

Audit trails for compliance

Every payment should log: who approved, when, under what rule, against which PO, with the invoice and proof-of-delivery attached. Tax incentive auditors, studio completion bond reviewers, and equity investors all request this data.

Top payment processing tools for production

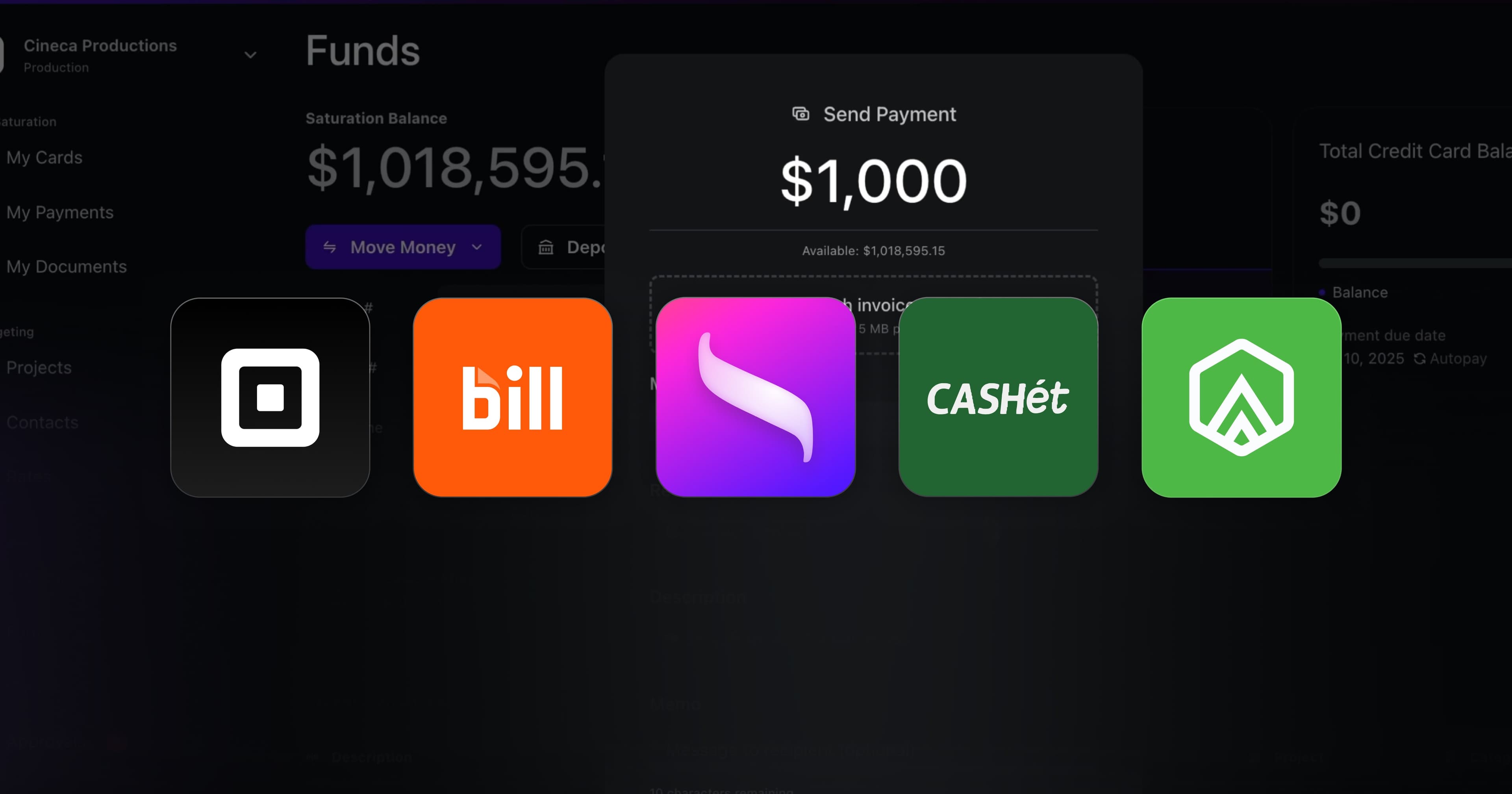

Saturation

Saturation Bill Pay integrates invoice intake, PO matching, approval workflows, and payment execution (ACH, wire, check) with production budgeting and banking. Payments auto-code to the budget line and flow into cost reports in real time. Multi-currency and SWIFT supported. See also Saturation Banking for the account layer.

GreenSlate

GreenSlate's production accounting and payroll platform includes invoice payment workflows integrated with their accounting and tax incentive modules. Best fit for productions on the full GreenSlate stack.

Entertainment Partners

EP's SmartAccounting platform includes invoice payment workflows tightly integrated with PSL payroll and SmartPO. Established, large-scale, and best for studio productions already in the EP ecosystem.

CASHét (EP)

CASHét (acquired by EP in 2025) offers a digital payment platform for production with card issuance, invoice payment, and crew expense tracking. Targets mid-size productions.

Bill.com and general AP

Bill.com, Melio, Tipalti, and Stampli are general SMB accounts payable tools. They handle invoices and payments competently but are not production-specific. A production would need to map transactions to the production chart of accounts manually. Fine for production companies using them for corporate spend; not ideal for per-show operations. See our Saturation vs Bill.com comparison.

Stripe, Square, and payment gateways

Stripe and Square are payment acceptance tools (production company receives payment from a client) rather than payment disbursement tools (production pays vendors). Useful for production companies billing clients, not for paying crew and vendors.

How to roll out a payment stack

Picking payment tools is one step. Making them work together on a real production is another. A common rollout sequence:

- Map current payment workflows before changing anything. Who pays whom, by what method, how often, through which tool.

- Identify the 80-20. Typically 20 percent of vendor relationships generate 80 percent of payment volume. Prioritize those vendors in the first onboarding wave.

- Run parallel for 1 cycle. Keep the old payment tool active for ongoing vendors while new vendors onboard to the new platform. Prevents missed payments during transition.

- Train approvers before rollout. Approval speed is the main gate on vendor payments. If UPMs and producers are not ready, the stack bottlenecks.

- Set up reconciliation before the first payment cycle. Reconciliation gaps compound if the first week's payments are not matched to bank statements.

How payment tools fit the banking layer

Payments originate from a bank account. Production-native platforms like Saturation bundle the banking layer (see our production banking guide) with the payment layer, so the ACH, wire, or check moves directly from the production account to the vendor without a separate payment gateway. Platforms that separate these layers require connecting to a bank, scheduling payments, and reconciling bank statements manually.

Fee structures to watch

Payment tools charge in several ways. Understand what you are paying before choosing a platform.

- Per-transaction fees. Per ACH, per wire, per check. Typical ACH is free or 50 cents. Wires run $5 to $25 domestic, $25 to $50 international. Same-day ACH is usually an extra charge ($1 to $5).

- Monthly platform subscriptions. Fixed cost for the software, usually $100 to $500 per production per month.

- FX markup. On international wires, the spread on currency conversion. Mid-market rate is the baseline. Traditional banks mark up 2 to 3 percent. Good production platforms run 0.5 to 1 percent.

- Bounce and reject fees. $15 to $35 per failed ACH or check. These add up if vendor account info is bad.

- Card funding fees. For platforms that issue cards, the fee to fund the card from a bank account (often free for ACH, a percentage for instant funding).

For a production processing 500 vendor payments and $1M in card spend, the annual fee impact can range from $2K to $30K depending on the mix. Always model total cost on the actual payment volume, not the headline subscription.

Security and compliance standards

Any platform handling ACH, wire, or international payments should be SOC 2 Type II certified at minimum. Many also carry PCI DSS for card processing and ISO 27001 for international operations. Check the platform's trust center for current certifications.

Compliance and standards

For payment processing standards, see Nacha (the US ACH rules body) and The Clearing House RTP for real-time payment rails.

Frequently asked questions about production payment processing

Do I need separate payment tools for invoices vs crew vs payroll?

Usually yes. Payroll (W-2) goes through a payroll firm. Invoices and contractor payouts can go through a production finance platform (Saturation, GreenSlate, EP). Cards and crew reimbursements are typically handled by production card programs. The key is that these tools talk to each other so a production accountant does not reconcile by hand.

What is the difference between same-day ACH and RTP?

Same-day ACH settles within hours and can be recalled. RTP (Real-Time Payments) settles in seconds, runs 24/7 including weekends, and is final. For time-critical vendor payments, RTP is ideal where supported. Same-day ACH is broader coverage and cheaper.

How do payment tools handle international vendors?

SWIFT wires are the default for international vendor payments. Multi-currency accounts (holding USD, EUR, GBP, CAD, etc.) reduce FX costs for frequent international spend. Reputable platforms quote FX at or near mid-market rates. Watch for 1 to 3 percent markups from traditional banks.

Can payment tools integrate with my production bank?

Yes. Most platforms either partner with an FDIC-insured bank directly (Saturation, CineFi) or connect via API to traditional banks for ACH and wire initiation (Bill.com, Tipalti). Direct integration is faster and reduces reconciliation; API connections still require bank-side processing time.

What is Nacha and why does it matter?

Nacha manages the ACH network in the US. Their rules govern how same-day ACH works, what types of payments are allowed, and fraud controls. Payment platforms must comply with Nacha rules. The standards affect timing (cutoffs, settlement times) and limits (per-day, per-transaction).

Are payment tools SOC 2 compliant?

They need to be. Payment tools handle bank details, vendor tax IDs, and production financials. SOC 2 Type II is the compliance floor, with audited controls around access, change management, and data encryption.

Can one platform handle both US and international payments?

Yes, the better ones do. Saturation, Bill.com, Tipalti, and EP SmartAccounting all support domestic ACH, wires, and international SWIFT. Multi-currency is a differentiator; platforms that force everything into USD charge FX twice (sending and receiving).

What happens when a payment fails or bounces?

Reputable platforms auto-retry, notify the approver, and hold subsequent payments to the same vendor until the issue is resolved. Status is visible in the platform, not buried in a bank statement email. Bounce fees are typically $15 to $35 per failed payment and should be tracked.

Related posts

Ready to modernize your production finance?

Join thousands of production teams using Saturation to budget, track expenses, and manage payments.